Tiếng Việt

Tiếng Việt

Risk management is the process of identifying, controlling, and minimizing potential losses in trading and investing. Traders protect capital and maintain long-term profitability.

Moreover, the risk management process includes defining risk tolerance, position sizing, and setting stop-loss levels, ensuring every trade is controlled before execution.

The risk–return theory states that higher potential returns always come with higher risk, forming the foundation of all financial decision-making and portfolio management.

In practice, traders apply risk management by limiting risk to 1–2% per trade, using stop-loss and proper position sizing to avoid large drawdowns.

Additionally, professional traders use advanced risk management systems and certifications to optimize capital protection, combining data analysis and strict discipline to achieve consistent results.

In financial markets, risk management is a critical factor that determines whether you survive or get eliminated. No matter how good your strategy is, without proper risk control, all your profits can be wiped out after just a few trades. To improve your trading decisions, you should also master Forex Technical Analysis as a core skill.

What is risk management and why it matters in financial markets?

Risk management is the systematic process of identifying, analyzing, and mitigating potential financial losses within an active trading or investment portfolio.

Statistically, implementing strict risk protocols directly impacts long-term survival, as empirical data shows that maintaining a maximum drawdown threshold below 15% to 20% dramatically increases the mathematical probability of compound wealth creation over a multi-year horizon. Without these guardrails, any short-term trading edge is completely neutralized by the inevitable mathematical reality of a losing streak, making structured risk controls the absolute foundation of all successful market operations.

What is risk management in trading and investing?

In active trading and investing, managing risk refers to the explicit rules an investor enforces to protect capital from adverse price movements. It involves the precise mathematical calculation of position sizes, the strategic placement of hard stop-loss orders, and the diversification of asset classes to minimize systemic exposure. Instead of trying to predict where the market will go with 100% accuracy, a professional risk manager focuses entirely on controlling how much capital is lost when a trade inevitably moves against their expectations.

Understanding this operational definition highlights the stark operational differences between professionals and struggling market participants.

Why do most traders fail without risk management?

The primary reason over 90% of retail traders lose their capital within the first year is the mathematical asymmetry of financial losses, known as the “drawdown trap.” For example, if a trader loses 50% of their account equity, they do not need a simple 50% return to break even—they require a massive 100% return just to return to their starting balance. Without strict stop-loss rules and position limits, a single emotional, over-leveraged trade can easily wipe out months of consistent profits, causing psychological panic and subsequent account ruin.

To prevent these catastrophic drawdowns, professionals convert abstract protective theories into a structured, repetitive workflow.

How the risk management process works in practice?

The risk management process works in practice by executing a continuous, data-driven cycle designed to systematically neutralize financial vulnerability before it impacts the balance sheet.

In institutional firms, this process is structured as a mandatory 4-phase framework: Identification, Assessment, Mitigation, and Continuous Monitoring. By funneling every prospective market exposure through this standardized loop, an investor ensures that no single trade can ever expose the broader portfolio to uncalculated or unmanageable catastrophic events.

What are the key steps in the risk management process?

The institutional risk process relies on four tightly integrated sequential phases:

- Identification: Pinpointing the exact types of risk present in a trade, such as market volatility risk, liquidity constraints, or broker counterparty risk.

- Assessment: Quantifying the potential financial impact by calculating the exact distance to your stop-loss and multiplying it by your contract size.

- Mitigation: Executing defensive actions, which includes adjusting your position size downward or utilizing options contracts to hedge physical exposure.

- Monitoring: Continuously reviewing the open position as market conditions shift, trailing stop losses to lock in profits, or closing trades ahead of high-impact news.

Transitioning this corporate framework into a personal trading terminal requires a highly practical, rule-based approach.

How do traders apply this process in real trades?

In a live environment, an active chartist executes this process by calculating their exact Risk Per Trade (RPT) before clicking the buy or sell button. For example, if a trader identifies a setup on a major currency pair, they immediately locate the structural invalidation point on the chart to define their stop-loss distance in pips. They then use a position-size calculator to ensure that if that specific stop-loss is hit, the resulting loss represents exactly 1% of their total account capital, removing all emotional guesswork from the execution phase.

While a structured process keeps you safe in real-time, optimizing your parameters requires a deep look at classical financial theory and asset correlations.

Risk management theory and the risk–return relationship

Risk management theory establishes the mathematical and scientific foundation for modern portfolio optimization, dictating how capital must be allocated to achieve maximum efficiency.

The core tenet of classical finance states that risk and return are directly correlated, meaning that an investor cannot achieve higher yielding returns without systematically increasing their exposure to potential capital loss. By utilizing verified statistical models, professional risk managers learn to structure portfolios that maximize returns while keeping overall portfolio variance within strict, tolerable boundaries.

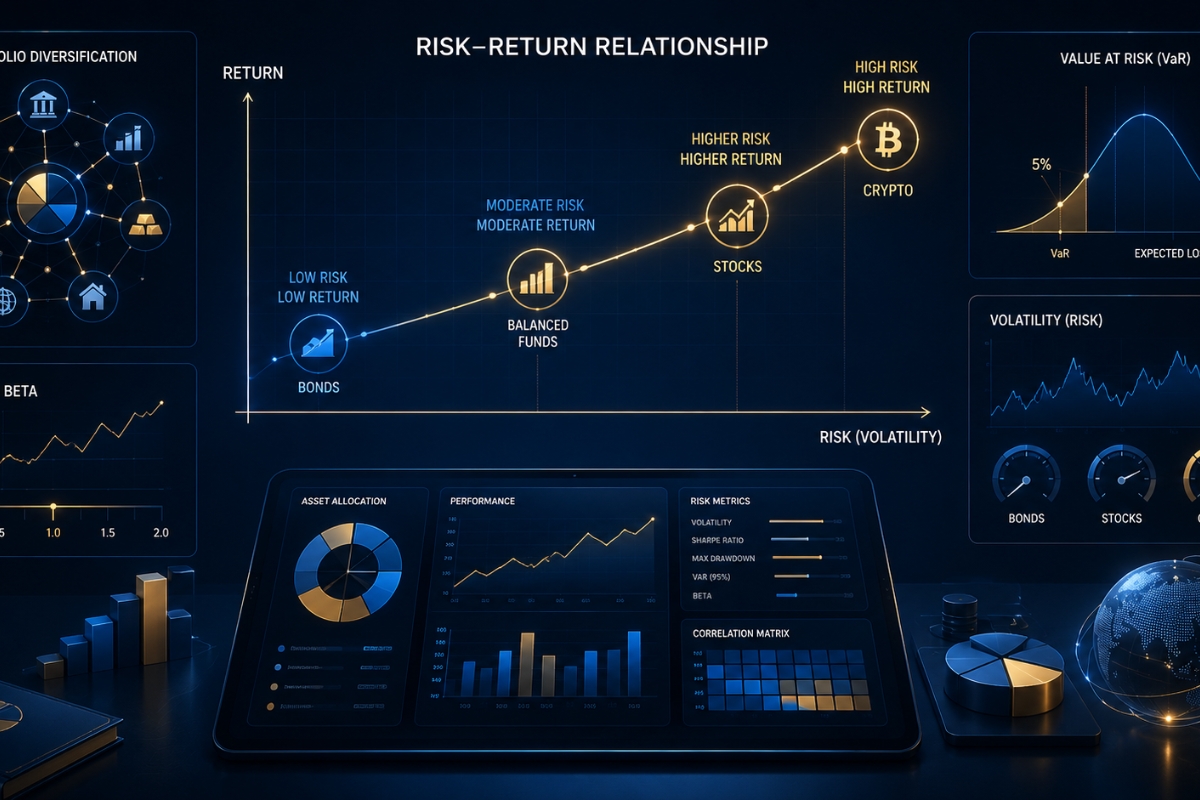

What is the relationship between risk and return?

The relationship between risk and return is a linear, positive correlation where the potential reward of an investment is mathematically bound to its underlying volatility and probability of failure. In efficient financial markets, low-risk assets like government bonds offer predictably lower yields, whereas high-risk assets like small-cap equities or cryptocurrencies demand a higher potential premium to compensate investors for capital vulnerability. A successful trading strategy does not seek to eliminate risk entirely, but rather to maximize the Sharpe Ratio, which measures the amount of excess return validated per unit of volatility.

To validate this relationship, institutional fund managers rely on time-tested academic frameworks that have shaped Wall Street for decades.

What financial theories support risk management?

Modern capital management is anchored by several groundbreaking academic frameworks:

- Modern Portfolio Theory (MPT): Developed by Harry Markowitz, MPT proves that an investor can significantly reduce portfolio risk through diversification—combining uncorrelated assets so that a decline in one sector is offset by a gain in another.

- Capital Asset Pricing Model (CAPM): This theory introduces the concept of Beta ($$\bet$$), which quantifies an asset’s systemic risk relative to the broader market, helping traders calculate the precise expected return required for taking on that exposure.

- Value at Risk (VaR): A statistical technique used to measure and quantify the maximum potential loss of a portfolio over a specific timeframe within a 95% to 99% confidence interval.

By converting these advanced theories into practical, everyday techniques, you can build a highly resilient investment strategy.

Applying risk management in trading and investment strategies

Applying risk management in trading and investment strategies requires translating complex mathematical formulas into highly actionable, daily trading rules.

This operational phase involves establishing non-negotiable execution parameters, defining strict account metrics, and utilizing advanced order types to protect your equity curves from unexpected liquidity shocks. When traders align these practical techniques with the high-performance execution environments found on platforms like MBroker, they create an unbreakable psychological and financial edge over the rest of the retail market.

What are the core risk management techniques?

To effectively defend your capital, your investment strategy should actively deploy three foundational pillars of risk control:

- The Hard Stop-Loss: An automated order placed with your broker that immediately liquidates your position at a predetermined price, preventing further capital damage.

- The 2% Rule: An ironclad rule stating that under no circumstances should a single trade cause a loss greater than a fixed, conservative percentage of your total liquid equity.

- A Minimum 1:2 Risk-to-Reward Ratio: Ensuring that your potential profit target is always at least double the distance of your defined stop-loss, guaranteeing that you can be wrong 50% of the time and still remain net-profitable.

To correctly execute these techniques, you must learn to calculate your exact position sizes based on your personal account parameters.

How much should you risk per trade?

Professional consensus dictates that conservative retail traders should risk between 1% and 2% of their total account balance on any single market setup. For instance, if you manage a trading account funded with $10,000, your maximum allowed risk per trade at a 1% allocation is exactly $100. If your technical chart setup requires a 50-pip stop-loss on a standard Forex pair, your position size must be restricted to exactly 0.2 lots, ensuring that a structural invalidation never triggers a significant psychological or financial setback.

Once you have mastered these foundational retail metrics, the final step toward institutional mastery involves exploring advanced industry standards and professional optimization protocols.

Advanced risk management and professional standards

Advanced risk management and professional standards represent the peak tier of financial control, utilizing complex data analytics, stress-testing simulations, and regulated certifications to govern institutional fund operations.

As global financial ecosystems become more complex due to high-frequency algorithmic trading and interconnected geopolitical risk factors, the demand for verified risk specialists has reached an all-time high. Adhering to these professional standards ensures that large-scale capital pools operate with absolute transparency and systemic resilience.

What is risk management certification and who needs it?

A professional risk certification is an elite, accredited designation that verifies an individual’s mastery of quantitative risk modeling, market regulations, and credit analysis. The most prestigious global standard is the Financial Risk Manager (FRM) designation, issued by the Global Association of Risk Professionals (GARP). This certification is highly sought after by portfolio managers, chief risk officers, compliance specialists, and institutional analysts who are legally responsible for managing multi-million dollar corporate funds or navigating complex banking regulations under Basel III standards.

Beyond individual credentials, professional trading networks utilize automated software infrastructure to keep their systems optimized.

How do professional traders optimize risk management systems?

Professional operators optimize their risk networks by running continuous algorithmic simulations and utilizing premium broker infrastructure. They subject their portfolios to rigorous Monte Carlo simulations and historical stress tests—modeling how their strategies would perform during historic black swan events like the 2008 financial crisis or the 2020 pandemic liquidity crash.

By combining these advanced quantitative filters with the ultra-low latency routing, tight spreads, and transparent execution structures championed on the MBroker homepage, professional chartists can safely eliminate execution slippage and protect their capital with absolute institutional precision.

In conclusion, Risk Management is not merely a secondary technical component of market analysis; it is the definitive core of sustainable financial survival. By mastering the 4-step risk process, respecting the mathematical laws of the risk-return trade-off, and strictly limiting your risk per trade to 1% to 2%, you can safely transform volatile market movements into a predictable, long-term commercial business model.

Thoren Vextal is a specialist in XM trading guides, offering practical insights and real-market experience to help traders improve their strategies and trading performance. Email: [email protected]